How to make the most of interest-free introductory offers (and avoid the traps)

Introduction

-If you’ve been browsing credit-card offers and come across terms like 0% APR, you might wonder: is this really a free ride? Or is it a trap in disguise? The truth is: a 0% APR credit card offer can be a powerful tool when used correctly—but it also comes with risks and pitfalls if you’re not fully prepared.

In this guide, we’ll walk through:

what exactly a 0% APR offer means

how to determine if you qualify and whether it makes sense for you

how to strategically use such a card (for purchases, balance transfers or both)

the key tricks to maximise value

the important “gotchas” to avoid

how to exit gracefully once the promotional period ends

By the end, you’ll have a clear roadmap to using 0% APR offers to your advantage—rather than falling victim to higher rates later.

Let’s begin by clarifying exactly what we’re talking about.What is a 0% APR Credit Card?

The meaning of “0% APR”

-When a credit card advertises “0% APR,” what it really means is: a 0% introductory or promotional interest rate for a limited period of time.

NerdWallet

+2

Lloyds Bank

+2

-That is, for that period you will not be charged interest on certain balances—if you abide by the terms.

What transactions it covers

-The promotional 0% rate may apply to different types of transactions:

Purchases: new charges you make on the card.

Citi

+1

-Balance transfers: moving an existing credit‐card balance (from another issuer) onto the new card.

NerdWallet

+1

-Sometimes both—but often the offer will cover one type and not the other.

NerdWallet

+1

-It’s essential to check the card’s terms so you know which transaction types are included.

The time‐limit

-The zero interest does not last forever. The offer normally covers a fixed period—common lengths are 6-18 months, sometimes up to 21 months or more depending on the issuer.

NerdWallet

+1

-Once the promo period ends, any remaining balance will automatically incur the card’s standard APR, which tends to be much higher.

Lloyds Bank

+1

You still have to make payments

-Even though you’re paying 0% interest, you still must make the minimum payment each billing cycle. Failure to pay on time can void the 0% deal, trigger a penalty APR, or both.

Citi

+1

-A common misconception: “I’ll just make the final one payment at end of promo” — the fact is you must pay each month. If you don’t, costs can skyrocket.

Why issuers offer these deals

-You might ask: why would a bank give you 0% interest for months? Because they hope to make money after the period ends—through high standard APRs, fees, new purchases at higher rates, or by capturing loyal customers.

As one source notes: “In a competitive marketplace, banks … will always compete for your business to keep you as a customer or attract you as a new client.”

Cardratings.com

So you have to treat this as an opportunity—but one that requires strategy.

Is a 0% APR Offer Right for You?

Before you jump in, you need to evaluate your own situation. Here are the key questions to ask.

Do you have a clear need?

-There are two main use-cases for 0% APR cards:

Large purchase: You plan to make a big purchase (e.g., home improvements, electronics, travel) and want to spread the cost interest-free for a period.

Debt consolidation / balance transfer: You already have high-interest credit-card debt and want to move it to an interest-free card so more of your payment goes to principal.

If you don’t have one of those needs, the benefit may be minimal—especially if you already pay off your cards each month.

Do you qualify?

-These offers tend to require good to excellent credit.

NerdWallet

+1

-You should also check that your credit limit will be large enough to accommodate your plan (either the purchase or the transferred balance). Many applicants find the approved limit is lower than expected.

NerdWallet

Can you plan to pay off the balance (or have a strategy) before the promo ends?

This is the critical part. If you know you’ll have the balance still at the end of the 0% period and you don’t have a plan, you may face a high interest rate. As one expert puts it: “The usefulness of a 0% deal depends on your habits.”

NerdWallet

A good rule: only use it if you are confident you can clear or significantly reduce the balance within the interest-free window.

-Are you disciplined with credit?

If you have a habit of overspending, making only minimum payments, or letting balances carry over, then a 0% deal could backfire. One source warns: “Be super organized and responsible; otherwise you will lose more than you will gain.”

milesearnandburn.com

-Also, using such a card may increase your credit‐utilization ratio (the percentage of your available credit you’re using), which can affect your credit score.

Citi

How to Choose the Right 0% APR Credit Card

If you’ve decided that you have a need and can execute a plan, the next step is selecting the right card. Here are criteria and comparison points.

- Determine what type of 0% offer you need

-0% on purchases only: Good if you have a large one-off purchase and intend to pay it off over time.

-0% on balance transfers only: Good if you already have existing credit-card debt you want to move.

-0% on both purchases & balance transfers: Ideal flexibility—but not always available, and terms may differ for each. For example length or fees may vary.

NerdWallet

+1 - Length of the promotional period

-Longer is obviously better—but longer often means tougher qualification or higher fees. Some cards offer 12, 15, 18 or even 21 months.

Yahoo Finance

Pick one that gives you adequate time to execute your payoff plan. - Balance‐transfer fees and other charges

-Often when you move a balance, you’ll pay a balance transfer fee, typically a percentage of the amount transferred. Even during the 0% period you may pay that fee upfront. Citi

+1

Also beware: some cards call “0%” but actually are deferred interest offers (where interest is accrued from day one unless you pay in full—see “gotchas” below).

- Standard (post-promo) APR

-When the 0% period ends, what will the standard APR be? You need to know that number because any remaining balance will begin accruing interest at that rate.

NerdWallet

If it’s very high, you must ensure you truly will finish the balance before then. - Credit limit and eligibility

-What credit limit will you need to accomplish your plan (purchase or transfer)? Some issuers may approve for less than you hoped.

NerdWallet

Also, check that your credit history is sufficient. - Additional perks, fees and rewards

-Although the interest offer is the drawcard, look at: annual fees, foreign transaction fees, rewards programs, ability to switch to a different card once the promo ends, etc. Sometimes a slight extra cost is worth it if the overall value is high. - The fine print

-Read the offer carefully: when the promo begins, when it ends, whether all transaction types are covered, minimum payments, whether new purchases will start to accrue interest if you carry a balance. For example, many cards exclude cash advances from 0% offers.

Citi

+1

It’s absolutely critical to understand the fine print.

Tips & Tricks – Using 0% APR Cards Strategically

Now we move into the more advanced strategies: how to use the card in a way that maximises value and minimises risk.

Tip 1: Use it for a planned large purchase

-If you have a major expense coming up (for example, a home renovation, appliance purchase, wedding, travel or educational cost), putting it on a 0% APR card can allow you to spread the cost interest‐free.

Here’s how to execute:

Know your timeline: let’s say you choose a card with 18 months at 0% on purchases.

Divide the cost by the number of months to know how much you must pay each month (plus any minimum payment). For example, $9,000 / 18 = $500 per month. As one guide suggests: “divide $10,000 by 18 months to see what you should pay every month.”

NerdWallet

Pay at least that amount every month (preferably more). Keep a calendar reminder for when the promo ends so you won’t be caught.

Do not make extra purchases unless you’re confident you can pay them off too—because new purchases may accrue interest or affect your payoff plan.

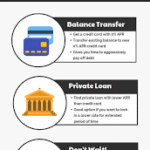

Tip 2: Use it for balance transfers to reduce high-interest debt

-If you already have credit-card debt at high interest, a 0% APR card for balance transfers can free up your payments to chip away at principal.

Strategy:

Apply for a card that offers 0% on balance transfers (preferably as long a term as possible).

Transfer as much of your high-interest debt as the card allows. Be mindful of any fees.

Focus all extra payments on that transferred balance so it outpaces the minimums.

Avoid adding new debt on the original cards you moved the balances from—this is key to making progress.

Towards the end of the promo, consider transfering the remaining balance to a new 0% card (if your credit allows) to extend the interest‐free time—but be careful about fees, approvals and credit impact.

milesearnandburn.com

Tip 3: Automate payments and track status

-One of the simplest yet most powerful tricks is: set up automatic payments so you never miss a minimum payment. If you miss a payment, you could lose the 0% offer entirely and get hit with penalty APRs.

NerdWallet

-Also: set a reminder halfway through the promotional period to assess your payoff progress. NerdWallet recommends this.

NerdWallet

Use budgeting tools to keep track of your progress and adjust as needed.

Tip 4: Try to pay more than the minimum

-Although you’re being charged zero interest, paying only the minimum each month means you’ll still carry a balance—and once the promo ends, interest will kick in on whatever remains. As one guide warns: “If you have to make a $10,000 purchase … divide it … and pay more than the minimum each month.”

NerdWallet

-he larger the chunks you pay sooner, the less you’ll owe when the interest-free window closes.

Tip 5: Know when the promotional period ends and plan your exit

-This is critical. At the end of the 0% period, your remaining balance starts accruing interest. So:

-Check the statement or offer to know the exact end date.

Citi

-Before that date, you should either be completely paid off or have a transfer strategy in place.

-Some savvy users will apply for another 0% card before the first one ends, transfer the remaining balance, and thus extend their interest-free time. But each transfer may incur fees and affect credit.

milesearnandburn.com

Tip 6: Consider the credit-score impacts

-Using a 0% APR card isn’t risk-free for your credit score. Some points:

-Opening a new credit card triggers a hard inquiry on your credit file – may temporarily lower score.

NerdWallet

-Carrying a large balance (even at 0% interest) increases your credit-utilization ratio (balance divided by credit limit) – this can hurt your score.

Citi

-If you transfer debt, closing old cards (or leaving them unused) may affect your credit history length and available credit.

-Therefore: keep the card open (if there’s no annual fee) after you’ve paid the balance if possible – this helps your credit profile.

Tip 7: Use the deal as leverage

-Even if you don’t end up using the card for a large purchase or transfer, you may find simply qualifying for a 0% APR offer gives you bargaining power with your existing card issuer. One personal‐finance expert describes how they used it to negotiate lower rates.

Cardratings.com

-If your card issuer knows you have an alternative, they might offer you better terms to keep your business.

Tip 8: Don’t let the zero interest lull you into reckless spending

-It might feel like ‘free money’ when you’re not paying interest—but remember: you still owe the balance, and once the free period ends, you’ll owe interest on whatever remains. As one source caution:

“Be sure you track expenses and stick to a budget … don’t risk getting into debt and having to pay it off at a much higher interest rate.”

Cardratings.com

-If you cannot commit to paying it off, the convenience may cost you dearly.

-Common Pitfalls & How to Avoid Them

-Using 0% APR credit cards is not without hazards. Here are common traps, with solutions.

Pitfall 1: Thinking “0% means no payment due”

-As noted earlier: you must still make the minimum payment each month. If you miss it, you risk losing the 0% promo, incurring late fees, penalty APRs, and damage to your credit.

NerdWallet

-Solution: automate payments, set alarms and treat the card like any other loan: you owe monthly payments.

Pitfall 2: Underestimating the post-promo APR

-If you still carry a balance when the 0% period ends, you’ll begin paying interest at the regular rate—sometimes 20%-30% or higher. Worse, some offers carry deferred interest language (see next pitfall).

-Solution: plan your payoff schedule in advance, ensure you’ll clear it before the end—or have a strategy to transfer or pay off what remains.

Pitfall 3: Taking on new purchases you can’t afford

-Because you’re not paying interest, you might feel comfortable spending more—but if you add more charges before finishing your plan, you risk extending the payoff period and paying interest later, or never finishing.

-Solution: treat the card’s promo period as a budgeted timeframe, and limit use to planned purchases (or better yet, avoid new purchases until the plan is done).

Pitfall 4: Deferred interest / store-card traps

-Some retail or store credit cards advertise “0% interest” but operate under deferred interest: if you don’t pay the entire balance by the end of the promo, you’re charged interest on everything from day one, not just the remaining balance. A recent study found 85% of store cards with “0%” offers use deferred interest.

Reuters

-Solution: check for the phrase “deferred interest” in the terms. Prefer general-purpose cards with true 0% intro APRs (not deferred interest) for clarity.

-Pitfall 5: Balance transfer fees, shorter promo periods for transfers vs purchases

-Some cards may have a longer 0% period for purchases but shorter for balance transfers—or vice versa. Also, balance transfer fees (e.g., 3% of amount) can reduce savings.

NerdWallet

+1

-Solution: compare not just the “0%” claim but both the period length and the fees. Do the math to see if it still makes sense.

Pitfall 6: Credit-utilization spike hurting your credit

-Even though you’re not paying interest, if you carry a large balance, your utilization ratio rises (balance ÷ credit limit), and that can harm your credit score.

Reddit

+1

-Solution: if you must carry a big balance, consider keeping unused new credit lines to maintain total available credit, or pay down aggressively. Avoid maxing out the card.

Pitfall 7: Letting the promo end without repaying or refinancing

-If you ignore the end date, you may suddenly see interest charges hit. This undermines the whole benefit.

-Solution: set a calendar reminder at the beginning when you track your plan. At the midpoint of the promo period, review progress and adjust.

NerdWallet

-Real-World Example: Strategy in Action

-Let’s walk through a hypothetical example to illustrate how this might play out.

Scenario:

-You have $12,000 of credit-card debt at 21% APR. You apply for a new credit card that offers 18 months at 0% APR on both purchases and balance transfers, with a 3% balance transfer fee. The standard APR afterward will be ~24%.

Steps:

-Transfer the $12,000 balance (you pay a fee of 3% = $360 upfront).

-From the start of the 18-month 0% period, you commit to paying at least $700 per month. Over 18 months you’ll pay $700 × 18 = $12,600—enough to clear the balance before the promo ends, with some buffer for the fee.

-You set automatic payments and track each month. You avoid making new purchases.

-At month 9, you re-check progress: you’ve paid $6,300; balance is $6,660 (including fee). You adjust the payment if needed to stay on track.

-By month 18 you’ve paid ~$12,600; you’re fully cleared. Because you made all minimum payments on time, you’ve retained your 0% deal and avoided the 24% APR.

-After payoff you keep the card open (no annual fee) to maintain your available credit and benefit your credit score.

-Result: You paid $360 in fee but avoided roughly ~$2,100 in interest (21% × ~$10,000 × ~1 year). You regained financial flexibility and improved your credit profile.

-While this is simplified, it shows how planning, discipline and execution matter.

-Advanced Tricks & Considerations

-For more sophisticated users, here are some additional tactics to consider:

Trick 1: “Balance-hop” strategy

-Some savvy credit-card users apply for a new 0% APR card before their current promotional period ends and transfer the remaining balance to the new card, thereby extending the interest-free timeframe. Reddit users often discuss this:

-“Yes. Assuming you get approved for another 0% card, you could theoretically keep moving the balance around …”

Reddit

-But caution: each transfer may require a fee, may impact your credit score (new inquiry, more accounts), and you may need to qualify each time. This strategy works best for users with strong credit and a disciplined plan.

Trick 2: Matching the promo offer to your cash-flow cycle

-For example, if you expect a large business expense or tax payment in 12 months, you could apply for a 0% purchase card with a 15-month promo. That gives you breathing room. Similarly, if you anticipate a bonus or windfall, you could plan to pay the balance at that time.

-The key: synchronise your expected cash-flows with the card’s promo timeline.

Trick 3: Use the freed‐up cash flow for savings or investment

-During the 0% period, your interest cost is zero—but you’re still making payments. If you arrange the payments so that you free up some cash each month, you can put that into a high-yield savings account or investment until the card is paid off. Some Reddit users explore this:

-“Open up a card with a 0% introductory APR, and then take the money that would be used to pay off the credit card and invest it …”

Reddit

-This is more advanced and carries risk—but if executed well, you essentially borrow at 0% while your money works for you. But keep in mind: if you fail to pay off the card, the full interest cost kicks in. There is risk.

Trick 4: Leverage sign-up rewards + 0% offer

-If you qualify for a card that offers both 0% intro APR and a sign-up bonus or strong rewards program, you can maximise value. Just ensure you don’t incur unnecessary debt chasing rewards—and be careful that new purchases are still paid off.

Trick 5: Keep the card open after payoff

-Once you’ve paid off the balance, don’t necessarily close the card. Keeping it open can help your credit history length and available credit (which helps with utilization ratio). Just make sure there are no high annual fees, or consider downgrading the card.

-Frequently Asked Questions (FAQ)

-Here are answers to common questions about 0% APR credit cards.

Q: How many 0% APR credit cards can I have?

There’s no official legal limit, but each issuer will evaluate your creditworthiness and may cap your total credit with them. Also, opening too many cards in a short time may negatively affect your credit score.

NerdWallet

Q: Does applying for a 0% APR card hurt my credit?

Any credit-card application triggers a hard inquiry, which may slightly lower your score temporarily. Also, carrying a new credit line and higher utilization can affect it. But if managed well, the net effect can be positive (less expensive debt, better utilization).

Q: What happens if I miss a payment during the 0% period?

You could lose the promotional rate, be subjected to the penalty APR, owe late fees, and your credit score may be harmed. This undermines the whole benefit.

Citi

+1

Q: Is the 0% rate truly “zero interest forever”?

No—only for the specified introductory period. After that, any remaining balance will accrue interest at the standard rate. That’s why you must plan.

Q: Can I still add new purchases to the card while the 0% period is going?

Yes (if the card allows purchases during the promo), but you must ensure you can still pay those new purchases + the existing balance so the payoff stays on track. Also check whether the new purchases are covered by the 0% rate (some promos cover transfers but not new purchases).

Q: Are there “hidden” catches?

Yes—common ones include: deferred interest offers (not true 0% APR), balance transfer fees, shorter promo terms for transfers vs purchases, high post-promo APRs, and credit-utilization impact. Always read the fine print.

Reuters

+1

When a 0% APR Card Isn’t a Good Idea

-There are times when it may be better to avoid pursuing a 0% APR offer.

-If you don’t have a clear plan to pay off the balance within the promo period.

-If you have poor credit and may not qualify (or may qualify but only for a low credit limit, making your plan fall short).

-If the standard APR after the promo is extremely high and you believe you’ll still carry a balance.

-If you’re likely to add new debt on the card and not control spending.

-If your goal is simply short-term consumption and you’re not committed to paying off in the window—this can backfire.

-In those cases, you may be better off choosing a rewards card you pay off each month, or paying down existing debt without a balance transfer.

Exit Strategy: What to Do When the 0% Period Ends

-The promotional period is not the finish line—it’s just a milestone. Here’s how to transition.

Step 1: Check remaining balance

-At least one statement before the offer ends, review how much you still owe. If you owe zero—great. If you owe some amount, you need to decide next steps.

Step 2: Fully pay off if you can

-If you’re able, pay off the remaining balance before the end date so you avoid any interest at the standard rate. This is the ideal outcome.

Step 3: Consider transferring remaining balance

-If you still owe a significant amount and your credit is still strong, you might apply for another 0% offer and transfer the remaining amount. But weigh the transfer fee and credit-score impact.

Step 4: Transition into regular credit-card usage (if appropriate)

-Once the balance is cleared, you might keep the card open, use it for small purchases you pay off each month, thereby building credit history and benefiting from any perks.

Step 5: Review the card’s standard rates and fees

-If the card has a high annual fee or very high standard APR, and you don’t plan to use the card much, you might product-change (switch to a no-fee card) or close it—but remember closing may affect your credit profile.

Final Thoughts

-A 0% APR credit card can be a smart financial tool when used with discipline, planning and strategic execution. Whether you’re tackling high-interest debt or financing a large purchase, the interest-free window gives you breathing room—but only if you stay committed to your plan.

Key take-aways:

-Only pursue an offer if you have a clear plan and can follow through.

-Know all the terms: what types of transactions are covered, how long the promo lasts, what fees apply, what the standard APR will be.

-Automate payments, monitor progress and don’t let the window expire accidentally.

-Avoid using the card as a blank cheque for new spending unless you can pay it off.

-Use the payoff period to build stronger financial habits, improve your credit score, and avoid carrying high-interest debt.

-In the right hands, a 0% introductory card can save hundreds or thousands of dollars in interest—and accelerate your path to financial freedom. In the wrong hands, it can become another high-interest debt trap.

-Before you apply, take a deep breath, run the numbers, set your budget, mark your calendar—and then act with intention.

-Here’s to making smart moves, avoiding interest, and staying in control of your finances.

Title:

0% APR Credit Cards – Tips & Tricks

Word Count:

794

Summary:

-This article directs the attention of customers to 0% APR credit cards and tips and tricks to be aware of.

Keywords:

-0% APR Credit Card, 0% APR Credit Cards

Article Body:

-Credit cards can be considered to be one of the many basic necessities of the modern world. Credit cards are available nowadays in abundance. One type of credit card specifically is the so-called 0% APR credit card. 0% APR credit cards were introduced in the late 1980�s and to this day has still proven to be one of the most sought-after credit card types available anywhere. As with all credit card types, there are a certain tips and tricks surrounding 0% APR credit cards that all potential card applicants should be made aware of.

With the help of a 0% APR credit card, it means that you need not only pay the outstanding balance; and what more you could even charge up to the limits without having to sustain any monthly interest charges. However, sometimes, one tends to think just how these credit card companies can afford to provide 0% APR credit cards, and make a profit out of it?

Although 0% APR credit cards may not comprise any monthly charges, it is sure to come with annual fees which you are obliged to pay for the privileges of a 0% APR credit card. These annual fees usually run from $15 to $20 or sometimes, even higher. Having a 0% APR credit card doesn�t mean that you can pay your dues whenever and whichever way you intend to. It IS necessary to make your payments on time, or else, you will have to pay for high overdue fees. For each late payment, the 0% APR credit card holder has to pay fees that may range from $20 to $40. With habitual late payments, these meager amounts may accumulate to a hefty total!

It should be remembered that 0% APR credit cards are usually offered for only a stipulated period of time. This credit card interest may hold good for only a fixed period of time, usually ranging from 3 up to 15 months. On the completion of this period, a higher rate of interest may come in vogue, usually 12% or higher. You could easily transfer any existing credit card balances to a new 0% APR credit card to get 0% interest on the transferred balance. In this way, the credit card holder has to pay less interest for a stipulated period of time, and thus get a chance to clear outstanding balances as quickly as possible.

When applying for a 0% APR credit card, it is always better to read the terms and agreements of the credit card. Not to overstate an obvious question, but why should one do so? Simply because many credit cards may come with a default rate wherein late payments not only incur a late payment fee, but it would also include a default rate that will be added to the annual percentage rate. This in turn doubles the figures on the existing balances and on the new purchases made on the card moving forward. Ouch!

One very important point to take into account when applying for a 0% APR credit card is to read all paragraphs of the agreement, otherwise known as the fine print. This is because though it is illegal for a credit card company to hide their fees and charges, it is nonetheless legal for them to mention these points in small print! The 0% APR credit card companies thus usually announce in large and bold print about their 0% APR but hide the facts that this is only for a limited period of time and any extra fees which might be included are done so in very fine print.

Another trick that is up the sleeve of 0% APR credit card companies is to install sky-high APR�s right after the amount of 0% APR balance transfers are paid down. In other words, the money you first pay to the credit card company is applied to the transfer, and any other purchases you make will be charged a high APR. Sometimes, credit card companies may also go to the extent of sending you a different card than the 0% APR credit card you had initially applied for. In this way, you are not allowed the 0% APR but a different card offer with different terms and conditions. The card issuers typically rationalize this behavior based on the card issuer determining that you do not meet the qualifications for a 0% APR credit card. Qualifications for a 0% APR credit card is usually found in the small print of the agreement, and is usually overseen by applicants!

It can thus be seen that though 0% APR credit cards do seem to be rather inviting, there are some loopholes and tricks to their use. As always, it is highly recommended to read the terms and conditions on the card application agreement for the 0% APR credit card, or any type of credit card application, thoroughly in order to avoid any future problems, headaches or financial surprises.

Tinggalkan Balasan